![]()

CIFC Self-Study Guide for Becoming an Canadian Investment Funds Course Exam Expert

CIFC Study Guide Realistic Verified CIFC Dumps

NEW QUESTION # 134

Maxine is a portfolio manager who 15 years ago, purchased 100 shares of Never2Tacky, a social media corporation for Aspirations Global Technology Fund. She purchased the stock when it was trading at $10. Last year, the peak market price was $120. Presently, it is trading at $99. News agencies are now reporting that additional regulations regarding social media companies are about to be agreed upon by G7 countries. Maxine is concerned the market value of Never2Tacky is going to drop. She buys a put option with an exercise price of $95 with an expiry of 9 months.

What type of strategy is Maxine using?

- A. Speculating

- B. Passively managing

- C. Hedging

- D. Modern portfolio theory

Answer: C

Explanation:

Explanation

A put option is a contract that gives the buyer the right, but not the obligation, to sell a certain amount of an underlying security at a specified price within a specified time frame. A put option increases in value as the price of the underlying security decreases, and vice versa. Therefore, buying a put option can be used as a hedging strategy to protect against downside risk or loss in the value of the underlying security. In this case, Maxine is using a put option to hedge against the potential drop in the market value of Never2Tacky due to the regulatory changes. If the price of Never2Tacky falls below $95, she can exercise the put option and sell her shares at $95, limiting her loss. If the price of Never2Tacky stays above $95, she can let the put option expire and keep her shares, paying only the premium for the option. Buying a put option is not speculating, as it does not involve taking a high-risk position in anticipation of a favorable outcome. It is also not related to modern portfolio theory or passive management, which are different concepts in investment analysis. References: Put Option: What It Is, How It Works, and How to Trade Them, Put Options: What They Are and How They Work, Put: What It Is and How It Works in Investing, With Examples

NEW QUESTION # 135

Jabir recently joined Prosper Wealth Inc. and is looking forward to being a Dealing Representative for the firm. Which of the following statements CORRECTLY describe when Jabir will be eligible to open new client accounts and sell investments?

- A. Upon passing the proficiency course

- B. Upon employment with the dealer

- C. Upon formal confirmation from the regulator

- D. Upon registration application by the dealer

Answer: C

Explanation:

Explanation

Jabir will be eligible to open new client accounts and sell investments only after he receives formal confirmation from the securities regulator that he is registered as a Dealing Representative. This is because registration is a legal requirement for anyone who trades securities or advises clients on securities in Canada, unless an exemption applies. Registration helps protect investors by ensuring that only qualified and competent individuals and firms can conduct securities related business. Jabir must also meet the proficiency, solvency, and suitability requirements for registration, as well as comply with the ongoing obligations of a registrant. Passing the proficiency course and being employed by the dealer are necessary but not sufficient conditions for registration. The dealer must apply for registration on behalf of Jabir and wait for the regulator's approval.

References: Canadian Investment Funds Course, Unit 1, Section 1.2

NEW QUESTION # 136

Which of the following are obligations on mutual fund dealing representatives imposed by The Proceeds of Crime (Money Laundering) and Terrorist Financing Act?

- A. confirming client identity each time before concluding any transaction

- B. enhancing public awareness of matters related to money laundering and terrorist financing

- C. record-keeping of large transactions, account-related information, and other relevant records

- D. reporting all financial transactions to the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC)

Answer: C

NEW QUESTION # 137

Leira has a marginal tax rate of 45% and may deduct $5,000 in registered retirement savings plan (RRSP) contributions on her income tax return. If she decides to use her available deduction and assuming this does not reduce her taxable income to a lower tax bracket, by how much will it reduce her tax payable?

- A. $5,000

- B. $2,250

- C. $0

- D. $4,500

Answer: B

Explanation:

Explanation

A registered retirement savings plan (RRSP) is a type of tax-deferred account that allows individuals to save for retirement. Contributions to an RRSP are deductible from taxable income, which means that they reduce the amount of income tax payable for the year. The amount of tax savings from an RRSP contribution depends on the individual's marginal tax rate, which is the tax rate applied to the next dollar earned. Leira has a marginal tax rate of 45% and may deduct $5,000 in RRSP contributions on her income tax return. If she decides to use her available deduction and assuming this does not reduce her taxable income to a lower tax bracket, by how much will it reduce her tax payable? To answer this question, we can use the following formula: $$(Tax savings = RRSP contribution \times Marginal tax rate)

NEW QUESTION # 138

Darryl has a diversified investment portfolio of mutual funds in a non-registered account with Investwell Mutual Funds, a mutual fund dealer. Darryl's diversified portfolio is composed of 3 mutual funds. Each mutual fund is currently worth about $100,000. The ABC Canadian Equity Fund has a total return of 6%, the DEF Bond Fund has a total return of 8% and GHI Global Equity Fund has a total return of 10%. Darryl wants to make an in-kind contribution to his registered retirement savings plan (RRSP) account. He has unused RRSP contribution room of $60,000.

From a tax-efficient viewpoint, which funds contribute in-kind to his RRSP account?

- A. Move the DEF Bond Fund to the RRSP.

- B. Move the GHI Global Equity Fund to the RRSP

- C. Move $20,000 from each of the three funds to the RRSP.

- D. Move the ABC Canadian Equity Fund to the RRSP.

Answer: A

NEW QUESTION # 139

Ken is a member of his employer's Defined Benefit Pension Plan (DBPP). Which of the following statements about Ken's plan is CORRECT?

- A. Income received from the plan is eligible for pension income splitting even if Ken retires before 65.

- B. Contributions to the plan do not result in a Pension Adjustment (PA) for Ken.

- C. The amount that Ken will receive at retirement is not guaranteed.

- D. The amount Ken receives in retirement depends on the performance of the investments he has selected within the plan.

Answer: A

Explanation:

Explanation

The statement that is correct about Ken's plan is option D. A defined benefit pension plan (DBPP) is a type of employer-sponsored retirement plan that promises to pay a specified amount of income to the plan member upon retirement. The amount of income is based on a formula that considers factors such as years of service, salary, and age. Income received from a DBPP is eligible for pension income splitting even if Ken retires before 65, meaning that he can transfer up to 50% of his eligible pension income to his spouse or common-law partner for tax purposes. This can reduce the overall tax payable by the couple if they are in different tax brackets. Therefore, option D is correct about Ken's plan. The other statements are not correct about Ken's plan. Option A is false because contributions to the plan do result in a Pension Adjustment (PA) for Ken, which is an amount that reduces his RRSP contribution room for the following year. Option B is false because the amount Ken receives in retirement does not depend on the performance of the investments he has selected within the plan; rather, it depends on the formula that determines his pension benefit. Option C is false because the amount that Ken will receive at retirement is guaranteed by the plan sponsor, unless the plan sponsor becomes insolvent or terminates the plan. References: [Defined Benefit Pension Plans | GetSmarterAboutMoney.ca], [Pension Income Splitting | GetSmarterAboutMoney.ca], [Pension Adjustment (PA) | GetSmarterAboutMoney.ca]

NEW QUESTION # 140

What information does Fund Facts provide to potential investors?

- A. What the mutual fund is currently investing in.

- B. The portfolio management strategy that is used.

- C. How to calculate the taxes owed from investment income.

- D. The remuneration paid to the Independent Review Committee.

Answer: A

NEW QUESTION # 141

The Mutual Fund Dealers Association of Canada (MFDA) has strict rules concerning conflicts of interest.

Which of the following is TRUE?

- A. Activities that do not relate specifically to your employer need not be reported.

- B. Gifts and benefits may be provided to a client if your employer is aware of the benefits and has given approval.

- C. Only actual conflicts must be reported to your employer. Potential conflicts need not be reported because they have not happened yet.

- D. Borrowing money from a client will always be acceptable provided there is a written contract detailing the nature of the agreement.

Answer: B

NEW QUESTION # 142

Which of the followings describes segregated funds?

- A. Segregated funds offer some protection of the capital invested but there is an added cost for the protection.

- B. Segregated funds flow through capital losses to investors because the investors are the owners of the underlying fund.

- C. Segregated funds are subject to securities regulation because they are distributed by mutual fund dealing representatives.

- D. Segregated funds have high returns, high management fees, and cannot be redeemed until the maturity date of the contract.

Answer: A

Explanation:

Explanation

Segregated funds offer some protection of the capital invested but there is an added cost for the protection.

Segregated funds are contracts issued by life insurance companies that invest in underlying funds, similar to mutual funds. Segregated funds have a maturity guarantee and a death benefit guarantee, which ensure that the investor or their beneficiary will receive a certain percentage of their initial investment, regardless of market fluctuations. However, these guarantees come at a cost, which is reflected in higher management fees and insurance fees than mutual funds. Segregated funds do not have high returns, as they depend on the performance of the underlying funds. Segregated funds can be redeemed before the maturity date of the contract, but they may be subject to early redemption fees or market value adjustments. Segregated funds do not flow through capital losses to investors, as they are not considered owners of the underlying fund.

Segregated funds are subject to insurance regulation, not securities regulation, because they are distributed by life insurance agents. References: Segregated Funds

NEW QUESTION # 143

Janine will celebrate her 71st birthday this year. She currently has a lot of money in a personal registered retirement savings plan (RRSP) and knows there are rules about what she can do with those funds. Which of the following is TRUE?

- A. She can purchase a registered term or life annuity.

- B. She can take the entire amount in cash, with no tax consequences because her RRSP funds were tax-sheltered.

- C. She can convert her RRSP to a registered retirement income fund (RRIF) this year or by December 31st of next year.

- D. She can convert her RRSP to a locked-in retirement income fund (LRIF).

Answer: A

NEW QUESTION # 144

Charlotte has received proceeds from a deceased family member's estate. Charlotte decides to visit Malik, who's a Dealing Representative at her bank. She tells Malik, she does not know much about trading ETFs, but she wants to invest in ETFs. Charlotte says she feels fortunate to have this money and that she's not worried about losing it because she never planned on having any of it.

What element of the Know Your Client (KYC) information has Malik been able to learn?

- A. Risk Profile

- B. Risk Tolerance

- C. Risk Capacity

- D. Risk Preference

Answer: D

NEW QUESTION # 145

Jehona is a Dealing Representative with Vista Wealth Investments Inc., a mutual fund dealer in Ontario and Nova Scotia. Jehona has reviewed her client Sokol's account and wants to adjust the holdings and re-balance the portfolio. Which of the following statements about Jehona's permitted activities is CORRECT?

- A. If Jehona wants to execute trades for Sokol's account, Sokol must provide his specific authorization before the trades are entered.

- B. If Sokol has given Jehona discretionary trading authority, Jehona can process trades in the account without Sokol's pre-approval.

- C. If Jehona wants to execute the trades without Sokol's pre-approval, Sokol must first appoint Jehona as his Power of Attorney.

- D. If Sokol has signed a Limited Authorization Form, Jehona can process the trades in the account without Sokol's pre-approval.

Answer: A

Explanation:

Explanation

The statement that is correct about Jehona's permitted activities is option B. According to Section 13.3 of National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations (NI

31-103), registered individuals must not engage in discretionary trading, meaning that they must not execute a transaction for a client's account without the specific authorization of the client before the transaction.

Therefore, if Jehona wants to execute trades for Sokol's account, Sokol must provide his specific authorization before the trades are entered. The other statements are not correct about Jehona's permitted activities. Option A is false because a Limited Authorization Form does not allow Jehona to process trades in the account without Sokol's pre-approval; rather, it allows Jehona to accept instructions from a third party authorized by Sokol, such as a spouse or a lawyer. Option C is false because Sokol cannot give Jehona discretionary trading authority, as it is prohibited by NI 31-103 for mutual fund dealers and their representatives. Option D is false because appointing Jehona as his Power of Attorney does not allow Jehona to execute trades without Sokol's pre-approval; rather, it allows Jehona to act on behalf of Sokol in legal and financial matters, subject to certain conditions and limitations. References: [Registration Requirements, Exemptions and Ongoing Registrant Obligations], [Discretionary Trading | GetSmarterAboutMoney.ca], [Limited Authorization Form | IFIC],

[Power of Attorney | GetSmarterAboutMoney.ca]

NEW QUESTION # 146

Which of the following is a rationale for a portfolio manager to use a passive portfolio management strategy?

- A. The manager believes he or she can outperform the market with his or her stock picking skills.

- B. The manager wishes to create capital gains in the mutual fund by frequently buying and selling stocks

- C. The manager does not believe in using benchmarks.

- D. The manager believes that as the markets are fairly priced, it would be futile to look for mis-priced securities.

Answer: D

NEW QUESTION # 147

One of your clients, Harry, has heard that he can defer paying tax on capital gains. He wants to know if what he has heard is correct and if so, how to defer paying taxes on capital gains.

What would you tell Harry?

- A. Harry should buy and sell investments actively.

- B. He should invest in mutual funds just before the dividend paying date to pick up the dividend.

- C. He should hold unprofitable investments as long as possible.

- D. He should hold profitable investments as long as possible.

Answer: B

NEW QUESTION # 148

Which of the following statements about capital gains distributions from mutual fund trusts is correct?

- A. Capital gains from mutual fund trusts are deferred until the investor exits the mutual fund.

- B. Capital gains distributions from a mutual fund trust are reported annually on a T3.

- C. Capital gains distributions are not a disposition and are therefore not taxable.

- D. Capital gains from mutual fund distributions are 100% taxable.

Answer: B

NEW QUESTION # 149

Dakota is a Dealing Representative with Harvest Wealth Inc., a mutual fund dealer. Dakota starts a marketing campaign to contact prospective new clients and increase sales with existing clients. Which of the following CORRECTLY describes activities that Dakota can engage in under her marketing campaign?

- A. Dakota can send promotional emails to clients who have opted in to receive commercial electronic messages (CEMs).

- B. Dakota can make telemarketing calls to clients who are listed on the National Do Not Call List

- C. Dakota can send promotional emails to clients who have opted into Harvest Wealth's Do Not Call List

- D. Dakota can make telemarketing calls to clients who have opted in to receive commercial electronic messages (CEMs).

Answer: A

Explanation:

Explanation

Dakota can send promotional emails to clients who have opted in to receive commercial electronic messages (CEMs). A CEM is any electronic message that encourages participation in a commercial activity, such as an email, a text message, or a social media message. Under Canada's anti-spam legislation (CASL), Dakota must obtain consent from the recipients before sending CEMs, either explicitly (e.g., by asking them to sign up for a newsletter) or implicitly (e.g., by having an existing business relationship with them). Dakota must also identify himself and his dealer, provide contact information, and include an unsubscribe mechanism in every CEM. The other statements are incorrect. Dakota cannot make telemarketing calls to clients who are listed on the National Do Not Call List (DNCL). The DNCL is a list of telephone numbers of consumers who do not want to receive unsolicited telemarketing calls. Under the Telecommunications Act, Dakota must register with the National DNCL operator, subscribe to the National DNCL, and avoid calling any number on the list, unless he has express consent from the consumer or an exemption applies. Dakota cannot send promotional emails to clients who have opted into Harvest Wealth's Do Not Call List. A Do Not Call List is a list of telephone numbers of consumers who do not want to receive telemarketing calls from a specific organization.

Under the Telecommunications Act, Dakota must maintain an internal Do Not Call List for his dealer and respect the requests of consumers who ask not to be called by his dealer. However, this does not mean that he can send promotional emails to those consumers, as that would violate CASL. Dakota cannot make telemarketing calls to clients who have opted in to receive commercial electronic messages (CEMs). Opting in to receive CEMs does not imply consent to receive telemarketing calls, as they are different forms of communication governed by different laws . Dakota must obtain separate consent from the clients before making telemarketing calls to them, either explicitly or implicitly. References: [Canada's anti-spam legislation], [National Do Not Call List]

NEW QUESTION # 150

What purpose does it serve for non-money market mutual funds to hold money market instruments?

- A. They are purchased by non-money market funds to satisfy the regulatory requirement of fund diversification.

- B. Money market instruments primarily generate investment income that provides investors with preferential tax treatment.

- C. They ensure that the fair market value of a mutual fund will not drop below a minimal market value.

- D. If the portfolio manager has an immediate need for cash, money market instruments are relatively easy to liquidate.

Answer: D

NEW QUESTION # 151

Your client, Kimberly has investments in both registered and non-registered plans. Which of the following investment strategies is best suited for Kimberly from a tax perspective?

- A. Include dividend paying investments in the registered plan and interest paying investments in the non-registered plan.

- B. Include interest paying investments in the registered plan and dividend paying investments in the non-registered plan.

- C. Include investments paying capital gains in the registered plan and foreign pay investments in the non-registered plan.

- D. Include domestic pay assets in the registered plan and foreign pay assets in the non-registered plan.

Answer: B

Explanation:

Explanation

According to the Canadian Investment Funds Course, different types of investment income are taxed differently in Canada. Interest income is fully taxed at the marginal rate, while dividend income is favourably taxed with a dividend tax credit. Capital gains are taxed on 50% of the gain at the marginal rate, and foreign income is subject to withholding tax. Therefore, a tax-efficient strategy is to include interest paying investments, such as bonds or GICs, in the registered plan, where they can grow tax-deferred until withdrawal.

Dividend paying investments, such as Canadian stocks or ETFs, should be included in the non-registered plan, where they can benefit from the lower tax rate and the dividend tax credit. Foreign income should also be avoided in the non-registered plan, unless it is held in a U.S. dollar account or a foreign currency hedged ETF, to reduce the impact of withholding tax and currency fluctuations.

References: 1: Canadian Investment Funds Course - IFSE Institute 2 (Unit 9: Retirement)

NEW QUESTION # 152

A client has $950,000 in his RRSP account and $550,000 in his non-registered account held in nominee name with Tradewell Mutual Funds.

In the event of his dealer, Tradewell Mutual Funds declaring insolvency, what is the total amount the client be eligible to receive from the Mutual Fund Dealers Association of Canada Investor Protection Corporation (IPC)?

- A. The client will be eligible for coverage of $950,000.

- B. The client will not be eligible for any coverage.

- C. The client will be eligible for coverage of $550,000.

- D. The client will be eligible for coverage of $1,500.000.

Answer: A

Explanation:

Explanation

The amount that the client will be eligible to receive from the IPC is $950,000. The IPC is a not-for-profit corporation that provides coverage to eligible clients of insolvent members of the Mutual Fund Dealers Association of Canada (MFDA). The IPC covers up to $1 million per account type per client for losses of securities, cash, and other property held by the insolvent member. The account types include RRSPs, RRIFs, TFSAs, RESPs, and non-registered accounts. Therefore, the client will be eligible for coverage of $950,000 for his RRSP account, which is the value of his securities and cash held by Tradewell Mutual Funds in his RRSP account. The client will not be eligible for any coverage for his non-registered account, as it is held in nominee name, meaning that the securities and cash are registered in the name of Tradewell Mutual Funds on behalf of the client. Nominee name accounts are not covered by the IPC, as they are not considered to be at risk in the event of insolvency. Therefore, option B is correct regarding the amount that the client will be eligible to receive from the IPC. The other options are not correct regarding the amount that the client will be eligible to receive from the IPC. Option A is false because the client will be eligible for some coverage, as his RRSP account is covered by the IPC. Option C is false because the client will not be eligible for coverage of

$1.5 million, as his non-registered account is not covered by the IPC. Option D is false because the client will not be eligible for coverage of $550,000, as his non-registered account is not covered by the IPC. References:

[IPC Coverage | IFIC], [IPC - Home], [IPC - Coverage]

NEW QUESTION # 153

Francis wants to redeem his US Asset Allocation Fund as he needs the money for a down payment for a home purchase. The current proceeds from the redemption are USD $27,859, and the current CAD/USD exchange rate is 0.7353.

How much will Francis receive in Canadian dollars when he redeems the Funds? Please round your answer to the nearest dollar.

- A. $42,861

- B. $35,859

- C. $37,888

- D. $36,698

Answer: C

Explanation:

Explanation

A is correct because Francis will receive $37,888 in Canadian dollars when he redeems the Funds. This is calculated by dividing the current proceeds from the redemption in US dollars by the current CAD/USD exchange rate and rounding to the nearest dollar. That is,

NEW QUESTION # 154

Ai Fen has recently become registered to sell mutual funds with Acadian Eastern Financial, a mutual fund dealer. Ai Fen determined that with her background of being a Chartered Financial Analyst, she can help people understand the nature of investing more easily than others in her field.

Which registration category will need to be prominently noted on Ai Fen's business card to comply with the

"holding out rule"?

- A. Investment Representative

- B. Registered Representative

- C. Chartered Financial Analyst

- D. Dealing Representative

Answer: D

Explanation:

Explanation

The holding out rule is a regulatory requirement that prohibits registered individuals from using any title or designation other than their registration category when dealing with clients or potential clients. The purpose of this rule is to prevent misleading or confusing representations about the qualifications, roles, and responsibilities of registered individuals. According to Section 4.4 of National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations (NI 31-103), individuals who are registered to sell mutual funds must use the title "dealing representative" when holding out to clients or potential clients.

Therefore, Ai Fen must prominently note "dealing representative" on her business card to comply with the holding out rule. The other options are not valid registration categories for selling mutual funds. Option B is a generic term that does not specify the type of securities that can be sold. Option C is a registration category for individuals who trade securities on behalf of an investment dealer. Option D is a professional designation that does not indicate registration status. References: [Holding Out Rule], [Registration Categories], [Registration Requirements, Exemptions and Ongoing Registrant Obligations]

NEW QUESTION # 155

On January 3, John invests $500 in the Blue Sky U.S. Equity Fund. On July 1 of the same year, he invests another $500 into the same mutual fund. Information about the net asset value per unit (NAVPU) at the time of each transaction is provided below. Given this information, what will be the value of John's investment on December 31 of this year (please ignore transaction costs and distributions)?

- A. $1,198

- B. $1,256

- C. $1,216

- D. $1,332

Answer: B

Explanation:

Explanation

The value of John's investment on December 31 of this year can be calculated by multiplying the number of units he holds by the net asset value per unit (NAVPU) on that date. Since John invested $500 on January 3 and $500 on July 1, he holds a total of 125.6 units (62.8 units from the first investment and 62.8 units from the second investment). Therefore, the value of his investment on December 31 will be 125.6 units x $9.55 NAVPU = $1,256.

References: Canadian Investment Funds Course, Chapter 2: Mutual Funds1

NEW QUESTION # 156

Solomon is a Dealing Representative who is excited about a new equity fund his dealer recently approved. He thinks investors will be attracted to the fund's historical performance. He has a prospective new client, Madira, who is 25 years old. Madira has invested in mutual funds before, but not with Solomon's dealer. She has made an appointment to open a new RRSP with Solomon's firm.

What does Solomon need to do to make this a suitable recommendation?

- A. Show from past fund performance, that mutual fund costs are not important if there are high returns.

- B. Identify how the proposed investment is in alignment with the investor's profile and holdings.

- C. Rely on the risk rating of the mutual fund when offering an investment solution.

- D. Match the past rates of return of the mutual fund with what is the anticipated rate of return.

Answer: B

Explanation:

Explanation

To make a suitable recommendation, Solomon needs to identify how the proposed investment is in alignment with the investor's profile and holdings. A suitable recommendation is one that meets the investor's needs, goals, risk tolerance, time horizon, and personal circumstances. It also considers the investor's existing portfolio and how the new investment would affect its diversification, performance, and risk. Therefore, option C is correct regarding what Solomon needs to do to make a suitable recommendation. The other options are not correct or sufficient to make a suitable recommendation. Option A is false because mutual fund costs are important regardless of the past fund performance, as they reduce the net returns and compound over time.

Option B is false because relying on the risk rating of the mutual fund is not enough to offer an investment solution, as it does not reflect the investor's return expectations, liquidity needs, tax situation, or personal preferences. Option D is false because matching the past rates of return of the mutual fund with what is the anticipated rate of return is not a reliable way to make a recommendation, as past performance does not guarantee future results and may not be consistent with the investor's risk tolerance or time horizon.

References: [Suitability | GetSmarterAboutMoney.ca], [Mutual Fund Fees | GetSmarterAboutMoney.ca], [Risk Rating | GetSmarterAboutMoney.ca]

NEW QUESTION # 157

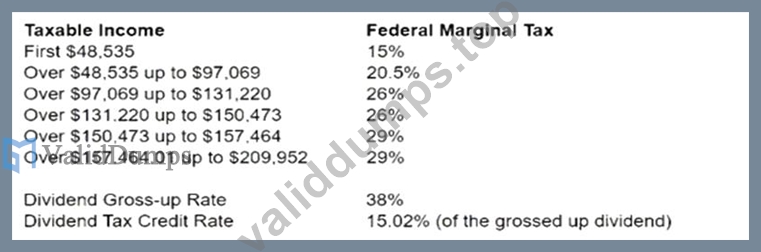

Last year Peter's earned income from employment was $50,000.

Last year, after receiving a $2 per share in dividends from 500 shares in ABC Inc., a publicly-traded Canadian corporation, he sold his shares. The sale resulted in a capital gain of $15,000.

Based on the tax rates mentioned above, what is Peter's net federal tax liability for the year? (Round to 2 decimal places).

- A. $9,193.69

- B. $9,953.30

- C. $9,696.15

- D. $9,113.53

Answer: A

Explanation:

Explanation

To calculate Peter's net federal tax liability for the year, we need to follow these steps:

Step 1: Calculate Peter's taxable income. This is the amount of income that is subject to federal income tax. It is equal to his earned income from employment plus his net capital gain plus his grossed-up dividend income. A net capital gain is 50% of the capital gain realized from selling an asset. A grossed-up dividend income is the actual dividend received plus a percentage of the dividend that reflects the corporate tax paid by the issuer. According to the image, the dividend gross-up rate is

15.02%. Therefore, Peter's taxable income is:

50000+0.5×15000+(500×2)×(1+0.1502)=68251.00

Step 2: Apply the federal tax rates to Peter's taxable income according to the tax brackets shown in the image. The federal tax rates are progressive, meaning that higher income is taxed at higher rates.

Therefore, Peter's federal tax before credits is:

0.15×(485350)+0.205×(6825148535)=11293.69

Step 3: Subtract the federal tax credits from Peter's federal tax before credits. A tax credit is an amount that reduces the tax payable by a taxpayer. There are two types of federal tax credits: non-refundable and refundable. Non-refundable tax credits can only reduce the tax payable to zero, but not below zero.

Refundable tax credits can reduce the tax payable below zero, resulting in a refund to the taxpayer. In this question, we assume that Peter only has two non-refundable tax credits: the basic personal amount and the dividend tax credit. The basic personal amount is a fixed amount that every taxpayer can claim to reduce their taxable income. According to this site, the basic personal amount for 2021 is $13,808.

The dividend tax credit is a percentage of the grossed-up dividend income that reflects the corporate tax paid by the issuer and avoids double taxation. According to this site, the federal dividend tax credit rate for eligible dividends in 2021 is 15.0198%. Therefore, Peter's federal tax credits are:

0.15×13808+0.150198×(500×2)×0.1502=2100

Step 4: Subtract Peter's federal tax credits from his federal tax before credits to get his net federal tax liability. This is the amount of federal income tax that Peter has to pay or has overpaid for the year.

Therefore, Peter's net federal tax liability is:

11293.692100=9193.69

Hence, option B is correct. References: Canadian Investment Funds Course (CIFC) | IFSE Institute, Federal Income Tax Rates for Canada - TurboTax Canada Tips, Capital Gains Tax in Canada | Wealthsimple, Dividend Tax Credit | TurboTax Canada Tips, Basic Personal Amount (BPA)

NEW QUESTION # 158

Pierre wants to discuss the merits of a specific mutual fund with his Dealing Representative, Simone. There are no trailer fees associated with this fund. Simone is familiar with the mutual fund that Pierre is referring to, which is not offered by her dealer. They schedule an appointment to further discuss his investment portfolio.

Which behaviour from Simone is ethical?

- A. Knowing Pierre does not like that her dealer's funds have trailer fees, she chooses not to discuss the relationship between trailer fees and MER while making comparisons.

- B. Simone's ability to keep her knowledge current on competitors' investment offerings shows that she is putting her client's interest first.

- C. While comparing Fund Facts of the different mutual funds, Simone points out that not only are the fund management expenses different but so are the investor profiles for each fund.

- D. When comparing her dealer's own mutual funds to the one Pierre discovered, Simone emphasizes the importance of similar net rates of return and minimizes the significance of management expense ratios (MERs).

Answer: C

NEW QUESTION # 159

......

Valid CIFC Exam Dumps Ensure you a HIGH SCORE: https://www.validdumps.top/CIFC-exam-torrent.html

CIFC Questions & Practice Test are Available On-Demand: https://drive.google.com/open?id=1w-KlHcT5uFlaLJDq_fWnELE-iLWVatlx